On May 15, Overstock (OSTK) filed a Form 4 with the SEC. The filing disclosed that Patrick Byrne, Overstock’s CEO and Chairman, had sold 500,000 shares of common stock in the open market. That revelation sent Overstock down about 15% on the day.

For me, going long Overstock has been a humbling experience. The thesis for Overstock was that the market had been focused on the blockchain venture business and was not fully appreciating the value of the eCommerce business.

Patrick Byrne had been quite outspoken about the company’s intention to sell or merge Overstock’s retail business with a more conventional retailer. He even went so far as to proclaim that he expected this to happen before the end of the first quarter of 2019.

The Original Overstock Thesis was as follows:

- The market is not valuing the retail arm of Overstock. On a comparable transactions basis, the value of the retail is bigger than the market cap of Overstock.

- The retail business is up for sale, thus a catalyst for a revaluation.

- Special Situation should play out in 1Q2019.

Obviously, this is not how things played out. Byrne, who has a history of overpromising and underdelivering, was not able to close a transaction in 1Q2019 nor has he been able to disclose any material developments on the sales process. In fact, the company has pulled back significantly on their communication regarding a potential sale, saying they will operate it as they will own it forever while openly discuss with interested acquirers.

In this article I attempt to answer the following questions:

- Is Patrick Byrne really the shareholders’ humble servant?

- Is Overstock at risk of a liquidity crisis?

- Has there progress in selling off the retail business? (spoiler: it might be)

- At what point is the retail business worth +$750 million?

- How much cash are the blockchain ventures consuming?

Nota bene: This article expresses my opinions on Overstock and is by no means investment advice. Caveat emptor…

- Sign up for Amazon Business Prime for your company

- Read Cryptocurrency Investment Research at Bitozi.com

- Earn up to 6% interest on your Bitcoin at Blockfi.com

Fighting Style Drift

The biggest challenge for an investor is to not get trapped by your own biases when things don’t play out as you anticipated. When the assumptions change, it’s pretty tempting to change your theses. Being wrong is hard and so often when the input changes, investors tend to update the equation and not the solution. This is generally called a thesis drift.

There’s a Wall Street joke about a technical analyst and a fundamental anlyst, engaging in a heated debate about investing over dinner. While making an animated case for value investing, the fundamental analyst accidentally swipes the meat knife of the table. Both analyst watch the knife fall to towards the floor where it sinks into the foot of the technical anlyst.

Fundamental Analyst: “Why didn’t you catch it?!”

Technical Analyst: “I don’t catch falling knives! Why didn’t you catch it?!”

Fundamental Analyst: “I thought it would go back up!”

In my case, I started buying Overstock at $22 in November 2018. I averaged down as the stock cratered and I’m now at an average purchase price of $13.90. The stock currently is trading at around $10.

The legendary economist John Maynard Keynes has a popular quote attributed to him. The story goes that Keynes was being challenged for changing his opinion on an economic subject, to which he replied: “When the facts change, I change my mind. What do you do, sir?“

In this article, I will blatantly report that the facts changed but I didn’t change my mind. My main argument for doing so is that the facts that changed are mostly facts that I discarded in my previous analysis.

At least until the next quarterly filings.

Why did Patrick Byrne sell shares?

The share sale disclosure sent some shareholders to the social media where they lambasted the transaction and demanded explanations from the CEO. The day after, Byrne issued a public statement which only seemed to further aggravate the Fintwit community.

What rubbed people the wrong way was the ending of the letter, where Byrne says: “I do not intend to ever give such an explanation again. I owe shareholders staying within the law and not making decisions based on inside information, not explanations of my life and projects outside Overstock.“

This statement from Byrne did come off as arrogant and disrespecting towards the Overstock shareholder base. Byrne is normally pretty nimble in terms of PR but this time, he lacked composure and disrespected his fiduciary duty towards his minority shareholders.

Irrespective of that, Byrne did announce his intentions after a previous share sale and in the latest annual report it’s clearly stated in black and white that he had shares pledged against personal liabilities:

Pledges of our shares by officers and directors and significant stockholders could have an adverse effect on us and on the market price of our common and preferred stock.

We do not prohibit or restrict our officers, directors, significant stockholders or others from pledging shares of our company owned by any of them, by holding them in a margin account or otherwise. Patrick Byrne, who is our Chief Executive Officer, a member of our Board and our largest stockholder (directly and indirectly through High Plains Investments LLC), has pledged approximately 1.9 million of the approximately 5.8 million shares he beneficially owns to one or more banks to secure a credit facility for High Plains Investments LLC and a personal loan. Any margin call or similar action by a lender that results in a forced sale of shares pledged by any of our officers, directors or significant stockholders could have an adverse effect on us and could have an adverse effect on the market price of our securities.

Although Byrne did not explicitly say so in his statement, it is probable that the share sales were a result of a margin call. As the excerpt above from the latest annual report (10-K) shows, out of the 5.8 million shares that Byrne held at the time of the filing, 1.9 million were pledged as collateral for other financial obligations.

On Owner Operators (in general)

According to one theory companies with Owner Operators outperform Agent Operators, in aggregate. One reason for this is due to owners having more Skin in the Game. Agent-operators tend to be incentivised to towards the upside. Owner-operators, on the other hand, have a significant part of their net worth tied up into the business. Hence, they should allocate capital better over time.

If we take this reasoning at face value, it should be a cause of great concern to see an owner-operator dump a significant portion of his shares. The problem with the owner-operator thesis is, as so often with theories, that the devil is in the details.

When an insider buys shares in the open market, it usually indicates that the insider is bullish on the risk-reward potential of the stock and the underlying business. Insider selling, on the other hand, can happen for various reasons. The insider might be paying off a loan, buying a house in the Hamptons, etc.

Similarly, when it comes to owner-operators, not all owner-operators are alike. Time and time again, we see owner-operators whose incentives diverge greatly from the minority shareholders. Eddie Lampert and the Sears Saga is a telling tale of that.

As Sears turnaround efforts failed to come to fruition and the company continued its downward spiral, ELS – Lampert’s hedge fund – funded the company with debt. This way, ELS was buying higher into the capital structure and was able to take control as the company went into bankruptcy. For common shareholders, bankruptcy meant total loss, for ELS it meant it could reorganize the capital structure while retaining control.

Personal liabilities of the owner-operator also play a part. When an operator has pledged his shares as collateral for a loan, the operator becomes more sensitive to the market price of the shares. Elon Musk, for example, has been reported to have pledged over 40% of his Tesla holdings as collateral for personal indebtedness.

In theory, an owner-operator that that faces a risk of a margin call is incentivized to maintain the share price even if it would mean sacrificing long term wealth creation. In simpler terms, the operator might be tempted to show higher accounting profits over investing resources into growth projects.

The Integrity of Patrick Byrne

The fact that Byrne had shares pledged was, to me, a fact that would stimulate Byrne to push for a sale of the retail arm as soon as possible. The fact that the intended sale did not occur and that Byrne was forced to sell shares at these prices can only indicate that selling the retail business is proving to be more difficult than they had anticipated.

Talking heads on social media have been criticising Byrne heavily for the way he has managed Overstock over the years. Many have lambasted him for selling shares and demanded that he relinquish his control of the company.

This reminds me a bit of the opening dialogue in Woody Allen’s Annie Hall, where tells a joke about two old women complaining about the quality of the food at a resort and at the same time, the size of the portions.

If you want Byrne out, him selling a big chunk of shares should be a positive event as he exposes himself to shareholder activism. Byrne currently controls 4,910,431 shares or about 13.9% of the shares outstanding.

There’s an old joke. Uh, two elderly women are at a Catskills mountain resort, and one of ’em says: “Boy, the food at this place is really terrible.” The other one says, “Yeah, I know, and such… small portions.”

– Alvy Singer in the opening scene of Annie Hall

Other investors, such as Mark Cohodes, have lamented the share sale, while at the same time defended the character of Patrick Byrne.

Byrne is – and has been for decades – a controversial figure. One could easily criticize many of the decisions he has taken over the years. One could also make the case that Byrne has been far too promotional in the way he comments publicly on the prospects of Overstock and the projects the company is involved in.

Nonetheless, the case for Byrne having participated in managerial capture would be a hard one to make. Byrne has throughout the years taken a comparatively modest annual salary in his role as CEO and Chairman of Overstock. In some years none and currently about $100,000 a year.

Furthermore, the equity compensation plan seems very fair towards shareholders with the average exercise prices of stock options issued to management at much higher levels that the current stock price.

Many owner-operated companies have a dual share structure with the operator holding super-voting shares, retaining absolute control even with a much lower economic ownership. Overstock has none of that.

Another trick would be to have the company incorporated in a state, less shareholder-friendly than Delaware, where most public companies list. The quality of Delaware courts and judges is the main reason why most public companies decide to incorporate there. Delaware has a special court, the Court of Chancery, to rule on corporate law disputes without juries.

Basically, the Delaware court is shareholder friendly as opposed to management friendly.

Overstock.com, Inc is incorporated in Delaware.

Looking at the Fundamentals

If you have read this far, you’ll note that our analysis so far has been devout of any discussion on fundamentals. To be true to the nature of this publication, I will make a fundamental case for why I’m still positive when it comes to Overstock.

In my previous analysis of Overstock, I performed a comparison of Overstock and its main competitor Wayfair. The problem with a comparison like that is that if you are arguing for reversion in multiples, you better be certain on which multiples will revert. In the case of Wayfair, the stock seems by most count overpriced, so it is just as likely that the valuation of Wayfair might lose some of its exuberance.

In any case, a comparison between Overstock and Wayfair is a tale of contrasts and fair value multiples could be somewhere in between. Since our initial coverage of Overstock, the company has filed the annual report for 2018 as well as the 10-Q for the first quarter of 2019. Let’s have a closer look.

Is There Liquidity Risk?

One of my favourite fundamental investors, Marty Whitman, said that the term risk is not very meaningful if there isn’t an adjective in front of it. Judging by comments online, one of the main perceived risks around Overstock is blowout risk.

This concern is not without merit. The company has been gushing cash into blockchain startups through its subsidiary Medici Ventures. At the same time, the Online Retail operations have been caught between a rock and a hard place. As the company competes against a very aggressive Wayfair, the Overstock.com has suffered from a hit to its Search Engine Optimization.

The problem began in early 2017 when Google implemented annual adjustments to its search algorithm. The problem persisted and prolonged into 2018. When you look at the magnitude of the hit, you realize that this was a real-life stress test that could kill most online businesses.

The effect of the SEO hit is very visible on the Overstock income statements in 2017 and 2018. In 2017 and 2018 combined, the company lost over $315 million. To put that into perspective, at the end of the first quarter of 2019, the company had a total stockholders equity of $209 million and a little less than $120 of cash on hand.

Is Overstock Retail still Competitive?

As shown above, Google made adjustments to its ranking algorithm in 2017 (as it does every year). Some of these changes seem to have caused a big hit in the overall ranking of Overstock.com. Most likely, the Google ranking algorithm started penalizing sites for some behavior that Overstock happened to be doing.

I think it is hard for people who are not familiar with eCommerce to grasp the severity of such a hit. Traffic through organic searches is immensely important to the sales funnel of an online retailer. It essentially feeds the rest of the sales funnel. If your organic traffic drops, there are fewer people to retarget, fewer social shares, fewer email signups, etc.

For Overstock, this meant that it became much costlier for the company to keep up the traffic to its website. To illustrate this point, take a look at the following table. From what it seems, the SEO hit may have cost Overstock over $200 million in additional marketing spending since 2017.

It might not be solely the SEO hit that is responsible for the increase in Sales and Marketing expenses. Patrick Byrne has stated that the Overstock tried to compete with Wayfair on advertising, which led to unprofitable acquisitions of customers.

Over the last years, Wayfair has invested significant amounts on multiple marketing strategies, Search Engine Optimization being one of them. It is possible that Overstock will not reach the previous levels of 7.15% sales and marketing expenses, as Wayfair has overtaken Overstock on SEO performance.

Can Overstock Retail Turn Profitable Again?

If we subtract the Sales and Marketing expenses from the Gross Margin of the online retail operations, we get to what is called the Contribution Margin. In the case of Overstock, the cost of goods sold includes the cost of products as well as fulfilment costs.

The contribution margin is, therefore, what you have left to spend after you made the sale. For an online company like Overstock, this includes technology and software spending. If a company’s contribution margin does not cover its expenses, then the operations are reliant on financing to fund its operations.

Based on the operating performance of Overstock through the latest quarters, it appears that the retail operations have cut the corner. Overstock has been trending towards its previous contribution margin levels. In the first quarter of 2019, contribution margin went above 10%.

But How Much Cash have Medici and tZero Burned?

Overstock started the Medici Ventures and tZero projects in 2015. Since then, accumulated increases in technology and administrative expenses are close to $250 million, compared to the cost level in 2014.

It is also worth noting that the technology costs on the income statement include the depreciation of capitalized technology spending.

During the first quarter of 2019, the retail operations showed signs of recovery, while tZero and Medici Ventures continue to be significant consumers of capital.

What caught my eye in this note to the first quarter filing are the increased operating expenses in the “other” segment. In the note on operating expenses, it says: “Corporate support costs have been allocated $12.6 million, $1.8 million, and $3.6 million to Retail, tZERO, and Other, respectively. Unallocated corporate support costs of $1.8 million are included in Other.”

Further down, on page 44 in the filing, in the management discussion of general and administrative costs, it says: “General and administrative expenses in Q1 2019 increased $477,000 compared to Q1 2018, primarily due to a $3.1 million increase in consulting expenses, a $2.6 million increase in legal fees, a $1.8 million increase in staff-related costs due to employee severance, and an $820,000 increase in audit and tax preparation fees. These increases were largely offset by a $6.9 million decrease in cryptocurrency losses and a $783,000 decrease in depreciation.“

A $3.1 million increase in consulting expenses is quite hefty for one quarter. It does not include any consulting expenses with regards to technology and development, which is a separate line item. The consulting expenses might be related to regulatory proceedings, such as the SEC investigation into the tZero token offering or work related to getting regulatory approval for the Boston Security Token Exchange to become a licensed national exchange.

You would, however, expect cost regarding the SEC investigation to fall under legal expense. Furthermore, the responsibility for getting regulatory approval for the Boston Security Token Exchange was in the hands of the Boston Options Exchange in the Joint Venture agreement.

Another possible reason for the increase in consultancy fees (caveat emptor, as this is pure speculation on my behalf) is that Guggenheim Securities have been hard at work during the quarter.

Overstock engaged Guggenheim in 2018 to explore strategic options for the retail business and find possible buyers. If the consulting expenses are mostly in the “Other” business segment and neither in the retail operations nor the tZero operations, it is plausible that Overstock is already in advance negotiations with potential buyers through Guggenheim.

What is Overstock Retail Worth?

Before we ask ourselves what the Overstock retail business is worth to a strategic buyer, we should take a step back and take note of the fact that it isn’t actually a retail business in the strictest sense of the word.

Consider the most recent balance sheet filed by Overstock. It has about $130 million in property and equipment. Property and equipment include internal-use software and website development costs. In fact, the majority of the property and equipment assets consist of internal-use software and website development costs.

At the same time, Overstock had roughly $13 million of inventories at the end of the quarter. For a company that did over 1.8 billion in revenues in 2018, that seems like an awfully low number. Compare that with a conventional retailer such as Bed, Bath & Beyond and the difference in business models is obvious.

What Overstock actually does is it connects over 4,000 third-party partners through its Supplier Oasis system. The Supplier Oasis system offers the partners a single integration point through which they can manage their products, inventory and sales channels, and also obtain multi-channel fulfilment services through Overstock’s distribution network.

Nearly all of Overstock’s retail revenues come from third-party partners and never touches any Overstock warehouse. As a result, the business model is very asset light compared to a conventional retailer.

At What Point is Overstock Retail Worth $750 million?

In my previous coverage of Overstock, the focus was on comparable transaction multiples. Needless to say, growth expectations and margins can have a big effect on revenue-to-value multiples. Therefore, it might offer some additional insights to look at the fundamentals of the retail business.

One question that we could ask ourselves is, for example, what would have to happen operationally for the Overstock Retail to be worth $750 million? Now, the first quarter saw a significant drop in revenues, so I’m going to assume that Overstock closes 2019 with a revenue of $1.7 billion.

The Gross Margin has been trending upwards and was 19.85 during the first quarter. Let’s assume 19.5% going forward. If we look at Sales & Marketing Costs from the 3 years prior to the SEO hit, 7.3% of revenue seems like a reasonable normalized rate for the retail operations.

Before the start of Overstock’s blockchain efforts, the company required about $80 million a year to run the retail business. Let’s assume we can make do with that. A strategic buyer would be able to remove duplicate administrative costs, such as costs from being a publicly traded corporate entity, so let’s assume that these costs could be taken down to $50 million annually.

Under these assumptions, Overstock Retail would produce an EBIT of $77 million on an annual basis. Assuming a 20% tax rate would translate to a Net Operating Profit after Tax (NOPAT) of just about $62 million. At 10x NOPAT, the business would be worth $620 million, at 15x NOPAT it would be $930 million. A multiple of 12.5x NOPAT would bring the value of the retail operations above $750 million.

Note that these assumptions don’t assume any growth. In fact, they assume revenues dropping by $100 million compared to 2018. They also assume a gross margin that is lower than the company recorded in the latest quarter. The only miracle that needs to happen is that the Sales & Marketing expenses return to normalized levels and that most of the technology costs increase over the last years are due to Medici Ventures and tZero.

“But what about the Balance Sheet?”, you might ask. Well, if we perform a crude separation of Overstock Retail and the Blockchain Business, we can measure a hypothetical Return on Net Operating Assets of the Retail Ops.

First of all, I’m going to assume that the retail business requires a cash buffer of $60 million, just to keep everything running smoothly and to counter any unforeseen hits to the business.

If we remove all balance sheet items that are not directly related to the retail operations and add the cash buffer we end up with about $40 million of working capital required to run the retail operations.

If we plug in the $62 million in NOPAT we came up with in our earlier exercise, the Retail Operations would be generating a 159% return on Net Operating Assets, under those assumptions.

What is the Value to a Strategic Buyer?

A strategic buyer isn’t “strategic” unless he can extract synergies from the acquisition. That’s the whole point of being strategic. In short, a strategic buyer is a buyer who can extract a higher utility out of an asset than the current owner.

To me, there are 3 types of strategic buyers for Overstock:

- A buyer that can tap into Overstock’s demand. To a conventional Speciality Retailer, acquiring Overstock would be a means to plug in a sales channel into its existing operations and push its own inventory into the sales funnels. If successful, this would allow the acquirer to increase the efficiency of its operations, for example by increasing inventory turns.

- A buyer that can tap into Supplier Oasis, Overstock’s supplier network. Companies that cater to a broad set of manufacturers, distributors or retailers as a marketplace for products, could cross-sell across the two platforms. A company like Groupon or QVC comes to mind.

- A buyer that can expand the Overstock model globally. Currently, Overstock’s sales (as well as the supplier base) is predominantly in the United States and Canada. A bigger and more global acquirer might be able to scale the business model internationally.

At this point, these thoughts are pure conjecture and it may well be that the increase in consulting fees during the last quarter has nothing to do with Overstock engaging Guggenheim Securities.

Does Overstock have any Brand Value?

One crude way for us to measure the brand values of various speciality retailers is by looking at direct brand searches online. Basically, how many times are people looking up the brand on Google on a monthly basis.

We could even take it further and create an index of brand value relative to the market value of those companies. We could do this by comparing brand searches to the market capitalizations of those companies. We could use enterprise value as well (equity + debt – cash) but as internet retailers are asset lighter, it might bias the index towards the internet retailers.

Needless to say, this is a very crude measure and should be taken with a grain of salt.

When we look at the brand searches and see how Wayfair has grown to 7.5 million brand searches compared to 1.8 million Overstock brand searches. Wayfair’s growth has not been limited to marketing and branding, as a large part of Wayfair’s growth has come from SEO as well.

This should raise some concerns for Overstock shareholders. If Overstock is falling behind Wayfair in terms of SEO, will they really be able to operate their business model at the historic marketing cost of 7.3% of revenues? If not, it would be a direct hit to the bottom line and would have a big impact on the actual value of the retail business.

There is no conclusive answer to this question, but I did do some sampling on some of Overstock’s most important keywords. You can try for yourself by looking at U.S. based search results for keywords such as “mattresses for sale”, “couches for sale”, “beds for sale” or “dressers for sale”.

It looks to me that Overstock is holding its ground and ranking above Wayfair on most of those keywords. This should indicate that the SEO performance of Overstock has, in fact, turned the corner.

But a few keyword samples won’t really tell the whole story and we might want to look at the overall performance of those two sites. Statistics from SimilarWeb will help in this regard.

From this data, it seems that Overstock earned back about 1 million monthly visits to its site, despite cutting down on ad spend. The company is still far behind the 25 million visits from December, but the trend is promising.

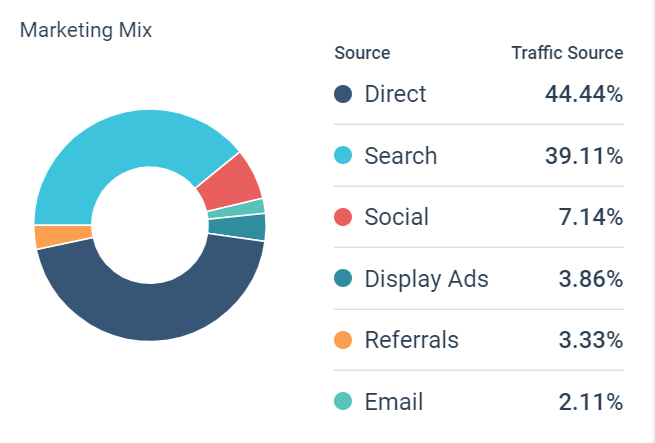

If we look at the traffic sources, we see the efficiency of the Overstock model. Over half of the traffic is coming through organic searches and over 40% is direct traffic. Less then 10% is coming through paid sources.

Wayfair, at the same time, has significantly more traffic to its site, with over 63 million visits in May. However, site visits seem to be trending downwards slightly.

If we look at the traffic sources of wayfair.com, we see that around 40% is coming from search and about 45% is coming directly to the site. Social, display ads and referrals account for roughly 14% of the traffic.

This, however, does not mean that the Wayfair business model is less efficient than the Overstock model. It all comes down to Unit Economics and Return on Incremental Invested Capital.

Unit Economics and ROIIC

The potential acquirers of Overstock Retail will base their valuations to some extent on the unit economics of the business model. The asset-light nature of the business model is what makes it valuable to a buyer that has the means to scale up the operations efficiently.

This is precisely the reason the management of Wayfair focus on unit economics in their communication to shareholders and the investment community. From their perspective, it is defensible to acquire business and market share at a loss if it means that the future acquisition of further business from the same customer comes at a lower rate. They are not acquiring the transaction but rather the customer.

Wayfair has been acquiring the business at a loss for years now but at the same time gaining significant market share. The logic is that at some point their market share is so large that they can turn down the marketing spend and reveal the true profitability of the business model. Because the profitability to the marketing investments is measured through the lifetime value of the customers, it masks the return on the incremental capital the company deploys into the business.

This thesis has allowed Wayfair to grow to a business that generated $6.7 billion in 2018. The winner-takes-it-all pitch has also created a company that has a negative book value of equity, while the market value of that same equity is over $13 billion. I’ll repeat. At the end of the first quarter of 2019, the book value of Wayfair’s equity was negative by $479 million. The market cap of Wayfair’s equity is currently $14 billion.

Can Overstock Raise Funds?

We could look at this from another angle. The gross margin that the online retailers generate from sales is primarily reinvested into sales & marketing and technology, such as website development. Therefore, the multiple of market cap to gross margin gives an indication of how cheap or expensive it is for the company to raise capital by issuing equity.

At current valuations, the common equity of Overstock trades at a multiple of a little less than 1x to its Gross Margin in 2018. At the same time, Wayfair’s market cap is a little less than 9 times its trailing Gross Margin.

This is a big problem for Overstock as the tZero operation alone is consuming probably around $50 million a year. Furthermore, if the Boston Security Token Exchange gets a go-ahead from the SEC, the project might require significant amounts of additional funding.

Raising capital through common equity of Overstock currently comes at a very high cost, given the current valuation. This means that Overstock needs to find alternative means of funding for the blockchain ventures. The big question is, can they do that?

Will Medici and tZero need more Funding?

In the exercise above we separated the retail business from the other assets and liabilities on the balance sheet. So, what about them?

What’s left are the operating assets of tZero, totalling about $63 million. Then there is $60 million in cash and cash equivalents, $2 million in cryptocurrency and about $48 million of equity in other companies.

On the liability side, you have the tZero security tokens which are recorded at $74 million on the balance sheet. These security tokens are essentially a royalty asset on the tZero business with 10% of all tZero revenues flowing to their holders.

Aside from that, there is only a $3 million debt security that relates to an Apple product repair business that Overstock took over in 2018.

The equity securities consist mainly of the blockchain focused startups and early staged ventures that Medici Ventures has been investing in over the last years. Of the $48 million of equity securities, about $32 million belong to Medici Ventures.

Aside from tZero and Medici Land Governance, Overstock is not a controlling investor in those ventures and is required to participate in future funding rounds of those companies. In fact, it is very plausible that Overstock could sell shares of those companies in a secondary market if the company needs liquidity.

Medici Ventures should be seen as a VC fund. The investments that that Medici has made are not consolidated in the Overstock balance sheet and the Medici does not have control ownership of those investments. This also means that Medici is not required to fund those operations and they are not required to participate in any future fundraising of those companies. If need be, there is likely a secondary market for some of those investments if Overstock needs to free up capital.

tZero, however, is a serious cash consumer at the moment for the company and with the lowered valuation of Overstock common stock, this will make it harder for Overstock to raise cash if they need it.

And they most definitely will.

Conclusion

- I believe that the share sale by Patrick Byrne has made the valuation of Overstock significantly undervalued.

- The reduced ownership of Patrick Byrne will make Overstock more vulnerable to shareholder activism.

- There is a possibility that the company is already in negotiations with potential acquirers of the retail business.

- Overstock Retail is a valuable asset, although it has been a hard sell due to the SEO hit it has been fighting since 2017. I do believe that Overstock Retail is running profitably at the moment.

- If the retail business returns to its previous operating performance, it will not even need growth to be worth at least $750 million to a strategic buyer.

- At the same time, Overstock is in a tight situation on a corporate level. The depressed valuation of its common shares will limit the options Overstock has to fund the development of the blockchain ventures.

- I remain long Overstock.

The Fundamental Finance Playbook is a publication dedicated to the Fundamental Research of Stocks and Security Analysis. We publish thoughts and opinions on individual publicly traded stocks as well as our thinking on methodologies for finance and investing practices in general.

All publications on the Fundament Finance Playbook are provided for informational and entertainment purposes only and do not constitute a recommendation to any particular security, a portfolio of securities, or an investing strategy.

Insider transactions are important to monitor however it doesn’t mean it’s a 100% signal as we saw steve jobs rip sold billions in shares before they grew 10 time+